This is a basic guide to the small salary big dividend method of rewarding yourself from your own company for the tax year ended 5 Apr 2024. If your company is only one of your income sources, alongside significant investment income, or a PAYE salary elsewhere, then you will need a tailor made strategy.

Let’s assume that your company is your main income and the other sources are relatively trivial. Your company is responsible tor maintaining a corporation tax reserve. Dividends can only be paid from the company’s post tax profit, so that means that the company tax reserve must stay in the company.

If you have no profit, then you can pay no dividend. Take care not to pay dividends out of investor funding, bank loans or your company tax reserve. Investor funding and bank loans are not “profit”. Your company tax reserve is not “distributable profit”.

When most of your income is from dividends then you will need a personal income tax reserve as well. Keep corporate stuff corporate and personal stuff personal. Maintain two tax reserves properly and then you’ll never get a shock when it’s tax payment time.

Follow this system precisely. Ensure bank transactions between your company bank account and your personal bank account follow this system accurately. If it’s not right then HMRC may decide that PAYE tax and National Insurance is due on all of your personal income. You definitely do not want that to happen.

For this process to be legitimate you must be a director/shareholder of a UK limited company.

Your salary is paid to you for the responsibility involved in “holding the office of director” and not for “work done”. It must be a separately identifiable bank transaction, and should be paid at the end of every calendar month.

All shareholders must receive dividends in direct proportion to their shareholding.

Beware of adverse consequences if you decide to take 100% of the dividend when you are not the 100% shareholder.

Other than salary, describe these amounts as “drawings” until the overall tax picture for the year is clear. The “dividend” is calculated later. Separate bank transfers are required in order to distinguish salary from drawings. In most cases that means setting up 4 separate payments at end of every calendar month. As Proactive does not hold any authorities on client bank accounts, it’s up to you to make the correct transfers at the correct time.

Basic rate taxpayers

For people whose monthly income does not exceed 4,188.

| Basic rate taxpayers | year ended 5 Apr 2024 |

| Monthly figures | |

| Salary | 758 |

| Primary “Tax Free” drawings (personal allowance) | 289 |

| Secondary “Tax Free” drawings (dividend rate band) | 83 |

| Tertiary drawings (max) liable to 8.8% tax | 3058 |

|

|

|

| Provided always that the monthly income does not total more than | 4188 |

| Put aside 8.8% of your tertiary drawings as a personal tax reserve. | |

Higher rate taxpayers

For people who need (and can afford) monthly incomes between 4,188 and 8,333.

| Higher rate taxpayers – 40% | year ended 5 Apr 2024 |

| Monthly figures | |

| Salary | 758 |

| Primary “Tax Free” drawings (personal allowance) | 289 |

| Secondary “Tax Free” drawings (dividend rate band) | 83 |

| Tertiary drawings liable to 8.8% tax | 3058 |

| Supplementary drawings (max) liable to 33.8% tax | 4145 |

|

|

|

| Provided always that the monthly income does not total more than | 8333 |

| Put aside 8.8% of your tertiary drawings as a personal tax reserve. | |

| Also put aside 33.8% of your supplementary drawings as a personal tax reserve. | |

Top rate taxpayers

For people who need (and can afford) monthly incomes in excess of 8,333.

There are graduated changes for annual incomes between 100,000 and 125,000 and the 45% rate of income tax also kicks in.

| Top rate taxpayers – 45% | year ended 5 Apr 2024 |

| Monthly figures | |

| Salary | 0 |

| Primary “Tax Free” drawings (personal allowance) | 0 |

| Secondary “Tax Free” drawings (dividend rate band) | 83 |

| Tertiary drawings liable to 8.8% tax | 3058 |

| Supplementary drawings (max) liable to 33.8% tax | 5192 |

|

|

|

| Additional drawings liable to 62.0% tax | excess over 8,333.00 |

| Put aside 8.8% of your tertiary drawings as a personal tax reserve. | |

| Also put aside 33.8% of your supplementary drawings as a personal tax reserve. | |

| And put aside 62.0% of your additional drawings as a personal tax reserve, because the personal allowance is withdrawn and that artificially creates an effective rate of tax of more than 60%. | |

For an independent view of this strategy have a look at this Unbiased report.

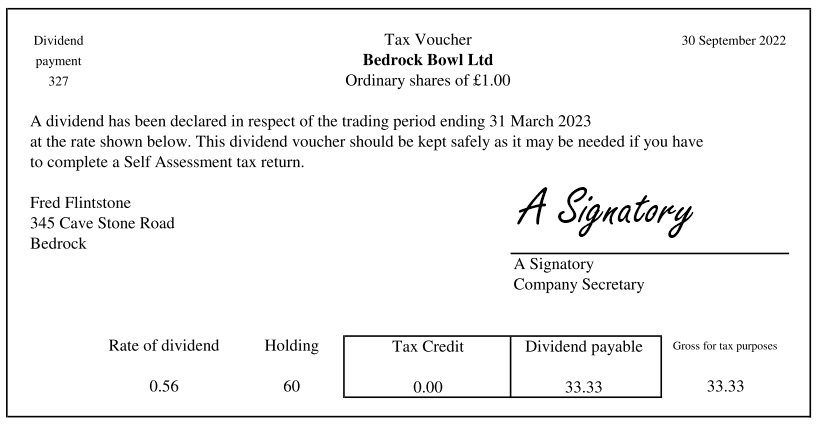

Find out more about dividend vouchers on this web site.

Is this legal?

Yes.

Lord Tomlin stated in the case of IRC vs Duke of Westminster (1936) 19 TC 490 every man is entitled, if he can, to order his affairs so that the tax attaching under the appropriate Acts is less than it otherwise would be.

The key thing is to keep this system in “order” and in compliance with the various Taxes Acts. If you deviate from the guidance above then you may find that your tax planning is not legal.