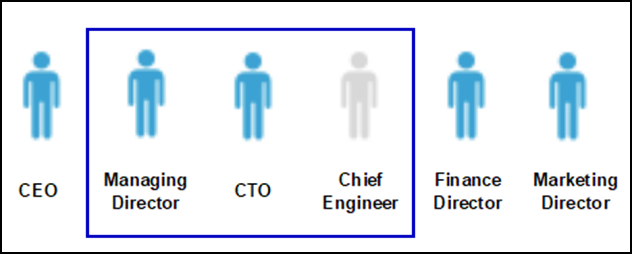

Key man insurance helps build a contingency in a case where one member of a board of directors dies. Typically it’s bought by larger companies (where there are multiple directors) for all the critical members of a board. Let’s say that London Time Machines Ltd has six directors (or senior staff) as follows:

At a board meeting they collectively agree that the business would struggle to operate if either the Managing Director, the CTO, or the Chief Engineer died. Sad as it might be, if any of the others died it’s not critical, so the “key man” label is attached to only three of them. London Time Machines Ltd takes out key man insurance naming these three individuals.

In the event that a key director dies, the policy is called in, funds are paid to the company, and the company continues to operate while urgently seeking a replacement for the missing director.

If you want key man insurance for a sole director limited company, and then you die, who is going to receive the funds and who is going to keep the business going?

For a business expense to be allowable, it has to be for the benefit of the business, not an individual. We cannot argue this with HMRC as it’s quite clear cut. It doesn’t matter what the marketing guff or the contract says, what matters are the reality and the brutal facts. The rules are set out in the Corporation Tax Act 2009 and UK GAAP.

When the sole director of a sole director limited company dies, then undoubtedly the business will cease. Before you take out key man insurance, first ensure that you have a team around you who can keep the business going. The insurance company will willingly take your money from you, but invariably HMRC will not grant tax relief to a sole director limited company for key man insurance.

Key man insurance is for mainstream businesses. If you want life insurance, buy life insurance privately. If you want a private pension then you need to weigh up the pros and cons of putting that through a business. Subject to limits, individuals and businesses can claim tax relief on pension contributions.